|

The correct answer is A

T=145/365 = 0.39726

d1 = [ln(27/30) + [.04 + .32/2](.39726)] / (.3√.39726)

= (-.10536052 + .0337671) / .18908569

= -.07159342 / .18908569

= -0.37863

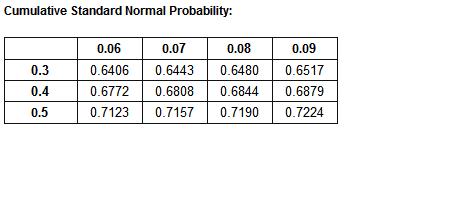

d1 = -0.37863 ≈ -0.38 N(d1) = 1 -0.6480 = 0.3520

d2 = -0.37863 - .3√.39726

= -0.37863 - .18908569

= -.56771569

= -.56772

d2 = -0.56772 ≈ -0.57 N(d2) = 1 - 0.7157 = 0.2843

PT = 30e-.04(.39726) (1-.2843) – 27(1-.352)

= (29.527056 × .7157) – 17.496

= 21.1325 – 17.496

p = $3.64 |

发表于 2009-6-26 10:06

|

发表于 2009-6-26 10:06

|