|

AIM 12: Define and compute a commodity spread.

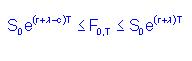

1、A hedge fund specializing in commodity related derivatives is considering a crush spread position using soybean and soybean oil futures contracts. Using the information in the table below, determine which of the following statements is correct.

|

< >> |

Soybeans |

Soybean Oil |

|

Spot Price |

$5.83/bushel |

$0.27/pound |

|

Storage Cost* |

0.63/bushel |

0.03/pound |

|

Convenience Yield* |

6% |

6% |

|

Interest rate* |

11% |

11% |

|

Time to expiration |

3 months |

6 months |

*Continuously compounded annual rates

A) The hedge fund should establish a long position in the soybean futures contract for no more than $6.91 and a short position in the soybean oil contract for no less than $0.29.

B) The hedge fund should establish a short position in the soybean futures contract for no less than $7.01 and a long position in the soybean oil contract for no less than $0.28.

C) The hedge fund should establish a long position in the soybean futures contract for no more than $7.01 and a long position in the soybean oil contract for no more than $0.29.

D) The hedge fund should establish a long position in the soybean futures contract for no more than $7.01 and a short position in the soybean oil contract for no less than $0.28. |

发表于 2009-6-26 14:22

|

发表于 2009-6-26 14:22

|

ffice" />

ffice" />