标题: Cfa level 3 关于duration [打印本页] 作者: leoye3602679 时间: 2014-4-22 10:40 标题: Cfa level 3 关于duration

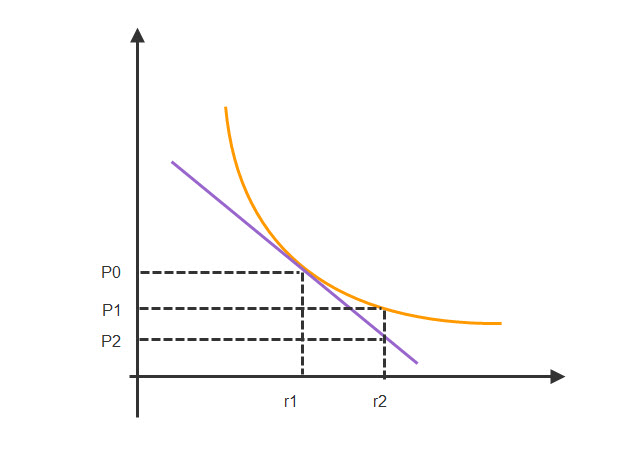

Notes 上说 “Due to linear nature of duration, which makes it underestimate the increase and overestimate the decrease in the value of the portfolio; convexity must also be considered. ” 如果不考虑convexity,假设duration是直线分布,应该是高估了增长好低估的下降吧,哪位能解释一下这句话?谢谢?作者: adjani.zhang 时间: 2014-4-22 11:41

图片附件: graph.jpg (2014-4-22 11:41, 23.67 KB) / 下载次数 0

图片附件: graph.jpg (2014-4-22 11:41, 23.67 KB) / 下载次数 0