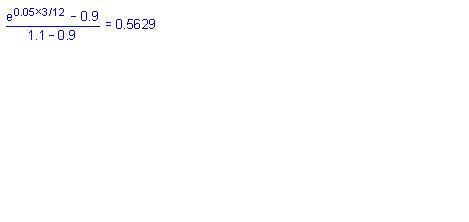

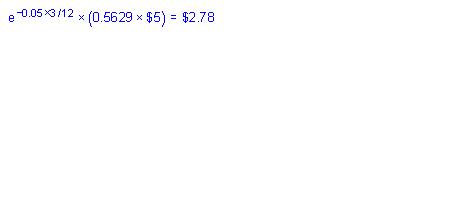

The correct answer is C

First, we need to calculate the size of an upward movement in the asset’s price as eσ√t = e(0.1825)(1) = 1.20. The size of a downward movement in the stock’s price is 1/1.20 = 0.83.

Next, we project the various paths the stock’s price can follow over the 3 year period. The stock has 4 potential ending values:

Suuu = $75 × 1.2 × 1.2 × 1.2 = $129.60

Suud = Sduu = Sudu = $75 × 1.2 × 1.2 × 0.83 = $89.64

Sudd = Sdud Sddu = $75 × 1.2 × 0.83 × 0.83 = $62.00

Sddd = $75 × 0.83 × 0.83 × 0.83 = $42.89

The only point at which the option finishes in the money is after 3 upward moves, which as a probability of (0.60)(0.60)(0.60) = 0.216.

The value of the option today is therefore ($129.60 - $90) × 0.216 × e(-0.05)(3) = $7.36. |

发表于 2009-6-25 13:55

|

发表于 2009-6-25 13:55

|