|

The correct answer is A

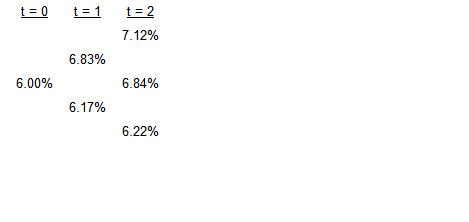

1、Calculate the payoffs on the call in percent for I++ and I+? (= I?+):

I++ value = (0.0712 ? 0.0625) / 1.0712 = 0.00812173.

I+? value = (0.0684 ? 0.0625) / 1.0684 = 0.00552228.

Remember that the payoff on the call value is the present value of the interest rate difference based on the raterealized at t= 2 because the payment is received at t = 3.

2、Calculate the t = 1 values (the probabilities in an interest rate tree are 50%):

At t = 1 the values are I+ = [0.5(0.00812173) + 0.5 (0.00552228)] / 1.0683 = 0.00638585.

At t = 1 the values are I? = [0.5(0) + 0.5 (0.00552228)] / 1.0617 = 0.00260068.

3、Calculate the t = 0 value:

At t = 0 the option value is [0.5(0.00638585) + 0.5(0.00260068)] / 1.06 = 0.00423893 0.00423893 × 100,000 = $423.89.

|

发表于 2009-6-25 14:11

|

发表于 2009-6-25 14:11

|